As a mortgage professional with years of experience, I’ve helped numerous clients navigate the complexities of FHA loans, including the often-misunderstood topic of MIP refunds. If you’re considering refinancing your FHA loan or simply want to understand your options better, this comprehensive guide to FHA MIP refund charts will provide you with everything you need to know.

Key Takeaways:

- FHA MIP refund charts show the percentage of the Upfront Mortgage Insurance Premium (UFMIP) that can be refunded

- Refunds are available for FHA loans refinanced within 3 years of origination

- The refund amount decreases over time, with no refund available after 3 years

- Understanding these charts can lead to significant savings when refinancing an FHA loan

What is an FHA MIP Refund Chart?

An FHA MIP refund chart is a tool used to determine how much of your Upfront Mortgage Insurance Premium (UFMIP) you can get refunded if you refinance your FHA loan within three years of the original loan’s inception. These charts show the percentage of the UFMIP that can be refunded based on how many months have passed since your original FHA loan was issued.

The FHA MIP refund is calculated by diminishing the refund amount over time, decreasing by 2 percentage points each month, and it can be applied towards new FHA loans such as FHA Streamline or cash-out refinances.

Understanding UFMIP and Why Refunds Matter

Before we dive into the refund charts, let’s quickly review what UFMIP is:

- UFMIP is a one-time fee paid at closing on all FHA loans

- It’s equal to 1.75% of the base loan amount

- It can be paid upfront or financed into the loan

For example, on a $200,000 loan, the UFMIP would be $3,500. That’s a significant amount, which is why understanding the potential for refunds is crucial. When refinancing an FHA loan, the upfront MIP payment is adjusted based on the MIP refund, which decreases over time, impacting the amount needed for the new upfront MIP payment.

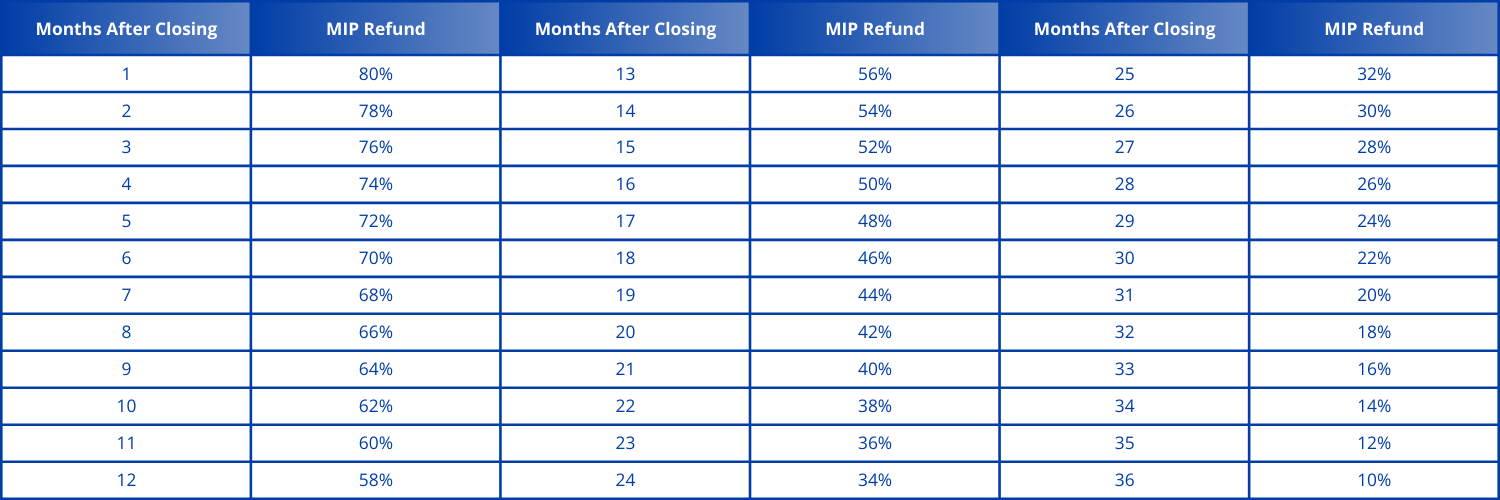

FHA MIP Refund Chart 2024

As you can see, the refund percentage decreases over time. After 36 months (3 years), no refund is available. The closing MIP refund is a percentage of the original MIP based on the duration of the mortgage.

When Does the FHA MIP Refund Chart Come into Play?

The FHA MIP refund chart becomes relevant in two main scenarios:

- FHA to FHA Refinance: If you’re refinancing from one FHA loan to another within 3 years of the original loan.

- FHA to Conventional Refinance: If you’re refinancing from an FHA loan to a conventional loan within 3 years of the original loan.

Current homeowners can utilize their previously paid MIP toward a new FHA refinance loan, which can provide financial benefits and involves specific calculations to determine refund amounts for qualifying refinancing transactions.

It’s important to note that the refund only applies to the UFMIP, not the annual MIP that you pay as part of your monthly mortgage payment.

Calculating Your Potential Refund

To calculate your potential refund:

- Determine how many months have passed since your original FHA loan was issued

- Find the corresponding refund percentage on the chart

- Multiply your original UFMIP by the refund percentage

For example, if you paid a $3,500 UFMIP 15 months ago and the refund chart shows 52% for 15 months, your potential refund would be:

$3,500 x 52% = $1,820

The FHA Streamline Refinance allows homeowners to modify their loans without requiring an appraisal and potentially receive refunds on mortgage insurance premiums.

Important Considerations About FHA MIP Refunds

While the potential for a refund can be exciting, there are several important factors to keep in mind:

- No Cash in Hand: The refund is not given to you in cash. Instead, it’s applied to the UFMIP on your new loan, reducing the amount you need to pay or finance.

- Refinance Timing: The timing of your refinance is crucial. Waiting even one month could reduce your refund percentage significantly.

- New UFMIP Required: When you refinance to a new FHA loan, you’ll need to pay a new UFMIP. The refund helps offset this cost but doesn’t eliminate it entirely.

- Conventional Refinance: If you’re refinancing to a conventional loan, you’ll receive the refund as a reduction in your payoff amount.

- Refund vs. Overall Savings: While a refund can be beneficial, it’s important to consider the overall cost of refinancing. Sometimes, the costs may outweigh the benefits of the refund.

There are two types of mortgage insurance premiums: upfront mortgage insurance premiums (UFMIP) and annual FHA mortgage insurance premiums (MIP). UFMIP is paid at the time of closing, while MIP is paid annually and impacts your monthly payments.

Strategies for Maximizing Your FHA MIP Refund

Here are some expert tips to help you make the most of potential MIP refunds:

- Time Your Refinance: If you’re considering refinancing, be aware of where you fall on the refund chart. Sometimes, waiting a month could cost you a significant portion of your refund.

- Consider a Conventional Refinance: If you’ve built up enough equity and your credit has improved, refinancing to a conventional loan could eliminate MIP entirely and still allow you to benefit from the UFMIP refund.

- Do the Math: Always calculate the total cost of refinancing against the potential savings, including the MIP refund.

- Stay Informed: Keep track of your original FHA loan date and stay informed about current interest rates and your home’s value.

Consistently making on-time mortgage payments can affect the potential for refunds on mortgage insurance premiums, thereby influencing the overall refinancing process.

How DSLD Mortgage Can Help

Navigating FHA MIP refunds and determining the best time to refinance can be complex. At DSLD Mortgage, we’re here to help. Our team can:

- Calculate your potential MIP refund based on your specific loan details

- Help you understand the pros and cons of refinancing, considering the MIP refund and other factors

- Guide you through the refinance process if it’s the right move for you

- Explore alternative options if refinancing isn’t the best choice

Conclusion: Knowledge is Power in FHA Lending

Understanding FHA MIP refund charts can potentially save you thousands of dollars when refinancing your FHA loan. However, it’s just one piece of the puzzle. The decision to refinance should always be based on your overall financial situation and long-term goals.

Remember, while MIP refunds can be beneficial, they shouldn’t be the sole reason for refinancing. It’s crucial to consider current interest rates, your credit score, how long you plan to stay in the home, and other factors before making a decision.

If you’re considering refinancing your FHA loan or have questions about MIP refunds, don’t hesitate to reach out to us at DSLD Mortgage. Our team of experienced professionals is here to help you navigate these complex decisions and find the best solution for your unique situation. Let’s work together to ensure you’re making the most of your FHA loan and setting yourself up for long-term financial success.

How much will your mortgage be? You can use DSLD Mortgage’s Mortgage Calculator to estimate your monthly mortgage payment.

Current mortgage rates holding you back? Don’t miss out on these deals! Buy a home with DSLD Mortgage and take advantage of our limited-time mortgage promotions.

Mortgage FAQs

Owning a home is a dream we help bring to life every day. You probably have a lot of questions, and that’s a good thing! Here are the answers to some of the most frequently asked questions we get, designed to make your path to homeownership as smooth as possible.

The three main reasons that can disqualify you from getting an FHA loan include having a high debt-to-income ratio, poor credit history, or insufficient funds to cover the required down payment, monthly mortgage payments, or closing costs.

According to FHA rules and guidelines, the property being financed must be occupied by the owner.

Begin Your Home Search with DSLD Homes

To get a feel for the lifestyle that awaits you in a DSLD Homes community, visit one of their communities throughout the Southern Region.

With a diverse selection of floor plans and communities to choose from, you’re sure to find the perfect fit for your lifestyle.

{kind=link}

{kind=link}